Buying a beautiful Cambridge Victorian or a classic brick rowhouse is exciting, but figuring out the financing can feel complex. Between historic rules, renovation costs, and lender requirements, you want a clear plan that supports both the purchase and the work. In this guide, you’ll learn how to fund a historic home in Cambridge, which loans and grants to consider, and how to keep your project on schedule. Let’s dive in.

What makes Cambridge homes “historic”

Cambridge regulates exterior changes that are visible from a public way in designated Historic Districts and Neighborhood Conservation Districts, and for Landmarks. That means some renovations need commission review and a certificate before work starts. You can confirm a property’s status and get free technical advice through the Cambridge Historical Commission. See the city’s overview of districts, permits, and help for owners on the Cambridge Historical Commission page.

- Learn more about historic districts, permits, and CHC guidance on the city’s site: Cambridge Historical Commission resources.

Financing paths that work for historic homes

Renovation loans that combine your purchase and rehab into one mortgage are often the best fit. They let your lender underwrite on the as completed value and fund draws as work progresses.

FHA 203(k) for owner occupants

FHA 203(k) finances the purchase and rehabilitation in one FHA insured mortgage. The Standard 203(k) covers larger or structural work and involves a HUD approved consultant. The Limited 203(k) fits smaller, non structural projects with lower caps. Funds are escrowed and released as milestones are completed. Review the program overview: FHA 203(k) rehabilitation.

Fannie Mae HomeStyle Renovation

HomeStyle is a conventional loan that bundles purchase or refinance with renovation funds. It is flexible, including energy and higher end improvements, and typically requires completion within 12 to 15 months. Lenders use an as completed appraisal to size the loan and will verify final completion. Explore details here: HomeStyle Renovation and see technical guidance on as completed appraisal and completion rules.

Freddie Mac CHOICERenovation

Freddie’s CHOICERenovation also combines purchase or no cash out refinance with renovation dollars. The program supports broad scopes of work, and CHOICEReno eXPress streamlines smaller projects. Funds are escrowed with inspections and completion certification. Read FAQs: CHOICERenovation and CHOICEReno eXPress.

Local grants and credits you can layer

Pairing the right mortgage with local assistance can reduce your out of pocket costs.

Cambridge Home Improvement Program (HIP)

The City’s HIP program, administered by Homeowner’s Rehab, Inc. and Just A Start, offers technical assistance and low interest or deferred payment rehab loans to income eligible owners of 1 to 4 unit homes. HIP often coordinates with the CHC for preservation scopes. Learn more: Cambridge HIP for homeowners.

Cambridge Preservation Grants

For eligible owner occupants, CHC’s CPA funded Preservation Grants can contribute to exterior restoration that returns original materials and appearance. The homeowner formula offers an outright grant up to $30,000, plus 50 percent of additional documented costs up to a $50,000 maximum disbursement, subject to program rules. See program details and how to apply: CHC Preservation Grants.

Lead paint credits and financing

Many Cambridge homes pre date 1978. Massachusetts provides a state tax credit for deleading expenses on residential units, with carryforward rules. There are also low cost “Get the Lead Out” financing options for eligible owners. Review the Massachusetts lead paint tax credit and financial assistance for deleading.

Tax credits for income producing properties

Massachusetts and federal historic rehabilitation tax credits generally apply to certified rehabilitations of income producing properties, not owner occupied primary residences. If you are considering a rental or mixed use project, review the Massachusetts Historic Rehabilitation Tax Credit and federal certification process.

Your step by step plan

Follow these steps to keep lenders, the CHC, and your contractor aligned.

-

Confirm historic status early. Call the Cambridge Historical Commission at 617 349 4683 to confirm designation and learn which exterior changes require a certificate. Start with the city’s guidance: CHC districts and permits.

-

Talk to CHC before you finalize scope. Early input can shape the design, materials, and timeline, which protects your budget and your lender’s schedule.

-

Get pre approved with a renovation savvy lender. Ask whether they deliver FHA 203(k), Fannie Mae HomeStyle, or Freddie Mac CHOICERenovation, and what documentation they require.

-

Build a detailed scope and bids. Lenders will need plans, itemized contractor bids, a realistic schedule, and a contingency reserve. For older homes, plan a 10 to 20 percent contingency.

-

Understand the appraisal. Renovation loans use an as completed appraisal, which reflects the value after the documented improvements. See how lenders evaluate this on Fannie Mae’s HomeStyle guidance.

-

Sequence permitting and loan deadlines. CHC hearings and certificates can add weeks or months. Renovation products usually require completion within 12 to 15 months, so align your milestones with commission review timelines.

-

Choose qualified contractors. Lenders often require licensed contractors, written contracts, and inspections for draws. Standard FHA 203(k) projects also involve a HUD 203(k) consultant. Program overview: FHA 203(k).

-

Confirm insurance coverage. Make sure your policy covers the completed value and any historic materials that affect replacement cost, like slate roofs or custom millwork.

Budgeting tips for older Cambridge homes

- Get a thorough home inspection and consider a preservation architect or structural engineer for complex projects.

- Prioritize safety and building envelope first, including roofing, masonry, wiring, plumbing, and any lead paint remediation.

- Use materials that meet CHC guidelines to avoid redesign or delays.

- Keep a cash cushion for surprises like hidden rot or outdated systems.

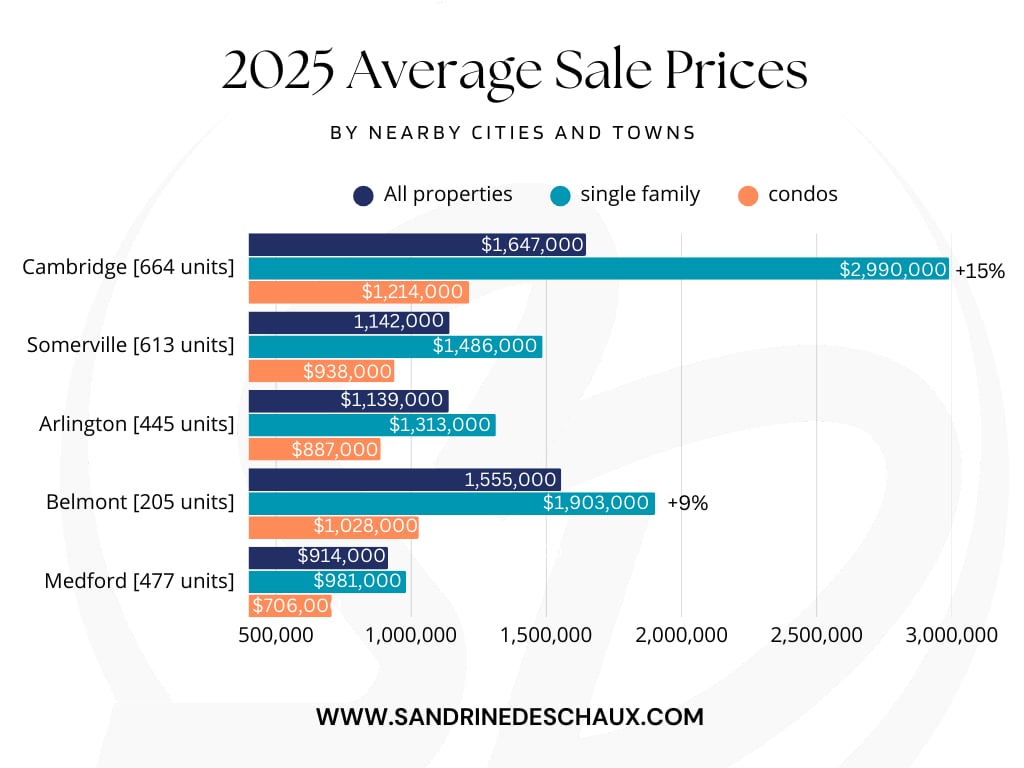

Cambridge market considerations

Cambridge home values are high relative to statewide and national medians, which can affect down payment size, loan limits, and appraisals. Renovation mortgages that rely on an as completed value can help you compete for a property that needs work and still fund the updates. The key is aligning your CHC approved scope, contractor bids, and lender timeline so your project stays on track.

Ready to take the next step?

If you are drawn to the character and craftsmanship of a Cambridge historic home, you deserve a financing plan that matches your vision. Let’s talk about neighborhoods, property condition, and a lending path that fits your goals. Connect with Sandrine Deschaux to map your next move with local, high touch guidance.

FAQs

How does Cambridge historic status affect financing and renovation timing?

- Historic district or landmark status can require commission review and certificates for exterior work, which adds steps and time that your lender will expect you to plan for. Start with the Cambridge Historical Commission resources and align your scope with their guidance.

Which renovation loan should I ask about for a Cambridge fixer upper?

- Owner occupants often start with FHA 203(k), while conventional buyers with strong credit consider Fannie Mae HomeStyle or Freddie Mac CHOICERenovation. Review FHA 203(k), HomeStyle Renovation, and CHOICERenovation to compare.

Can I use Massachusetts or federal historic tax credits on my primary residence in Cambridge?

- Generally no. State and federal historic rehabilitation tax credits target income producing properties, not owner occupied homes. See the Massachusetts Historic Rehabilitation Tax Credit for program scope.

Are there Cambridge grants that can reduce my out of pocket costs?

- Yes. Eligible owner occupants may combine HIP loans with CHC Preservation Grants for qualified exterior restoration. Start with Cambridge HIP and the CHC Preservation Grants page.

What lead paint assistance is available for older Cambridge homes?

- Massachusetts offers a state tax credit for deleading expenses and low cost “Get the Lead Out” financing for eligible owners. Review the lead paint tax credit and financial assistance options.

Thinking about selling a historic Cambridge home? Let’s plan your strategy., Contact Top Cambridge MA real estate agent Sandrine Deschaux with REMAX.