Shopping for a larger home in Cambridge and wondering if your mortgage will be considered “jumbo”? You are not alone. Many one-unit homes and luxury townhomes in Cambridge cross the line where a loan is no longer “conforming,” which changes how lenders underwrite and price your mortgage. In this guide, you will learn how to tell if you need a jumbo loan, what lenders expect, how appraisals work for higher-end properties, and smart strategies to compete with confidence. Let’s dive in.

What is a jumbo loan in Cambridge

A jumbo loan is any mortgage amount that exceeds the conforming loan limit for your county and property type. The Federal Housing Finance Agency, or FHFA, sets these limits each year. Loans at or below the limit can be delivered to Fannie Mae or Freddie Mac. Loans above the limit are typically underwritten as jumbos or kept on a lender’s portfolio.

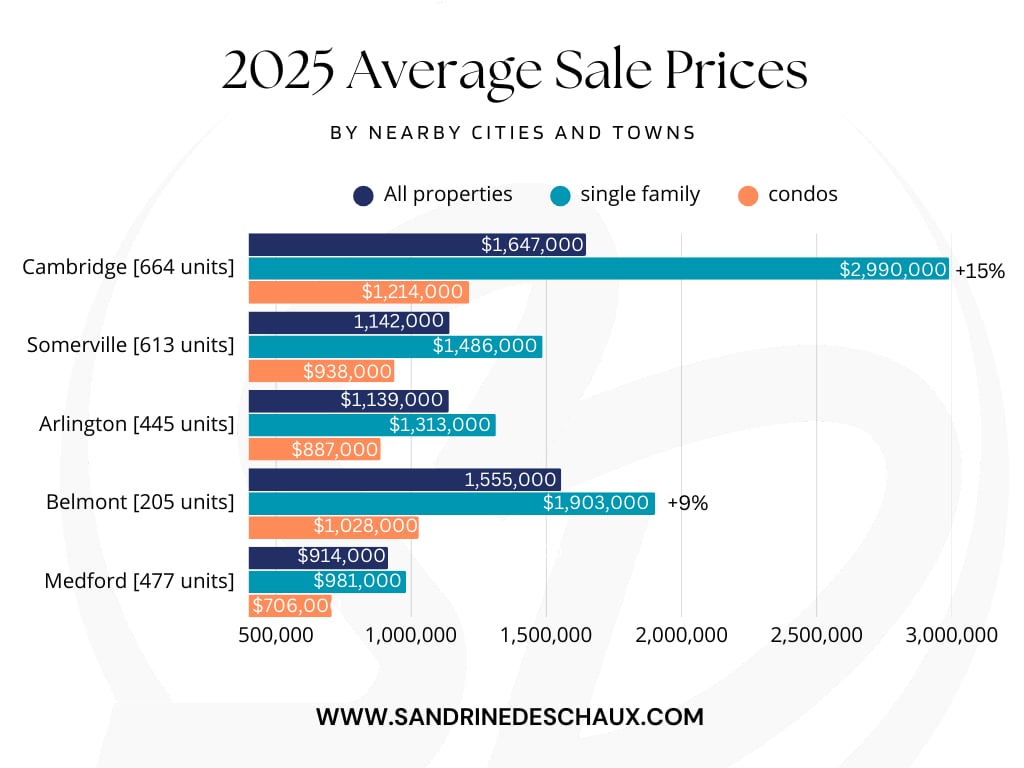

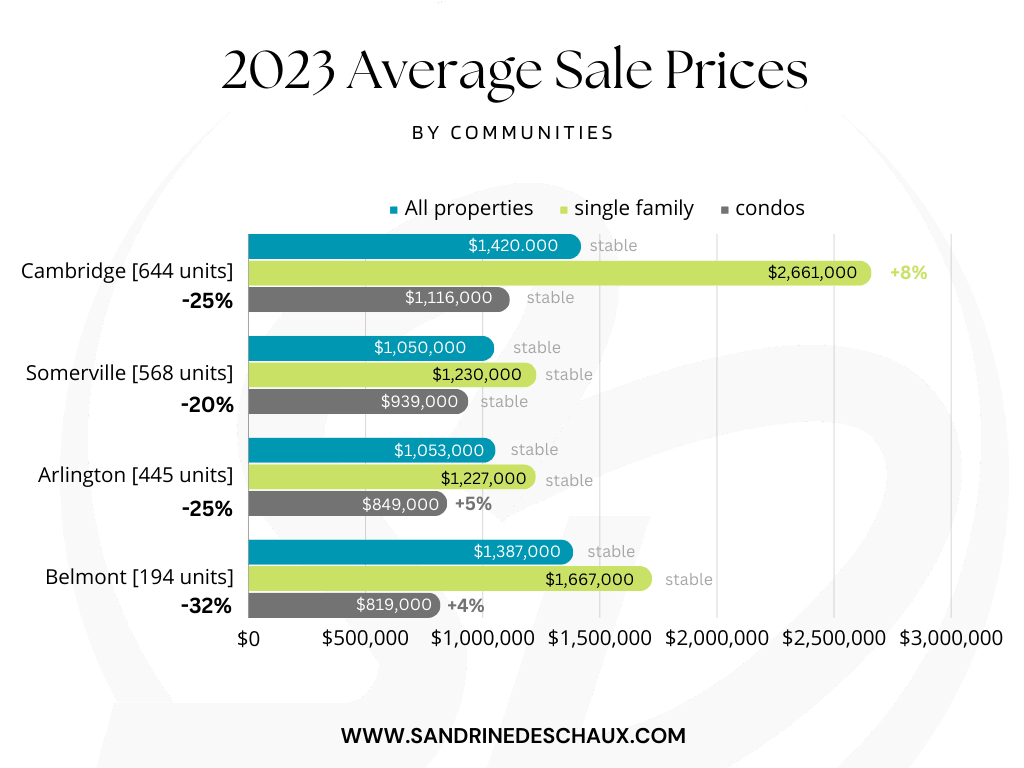

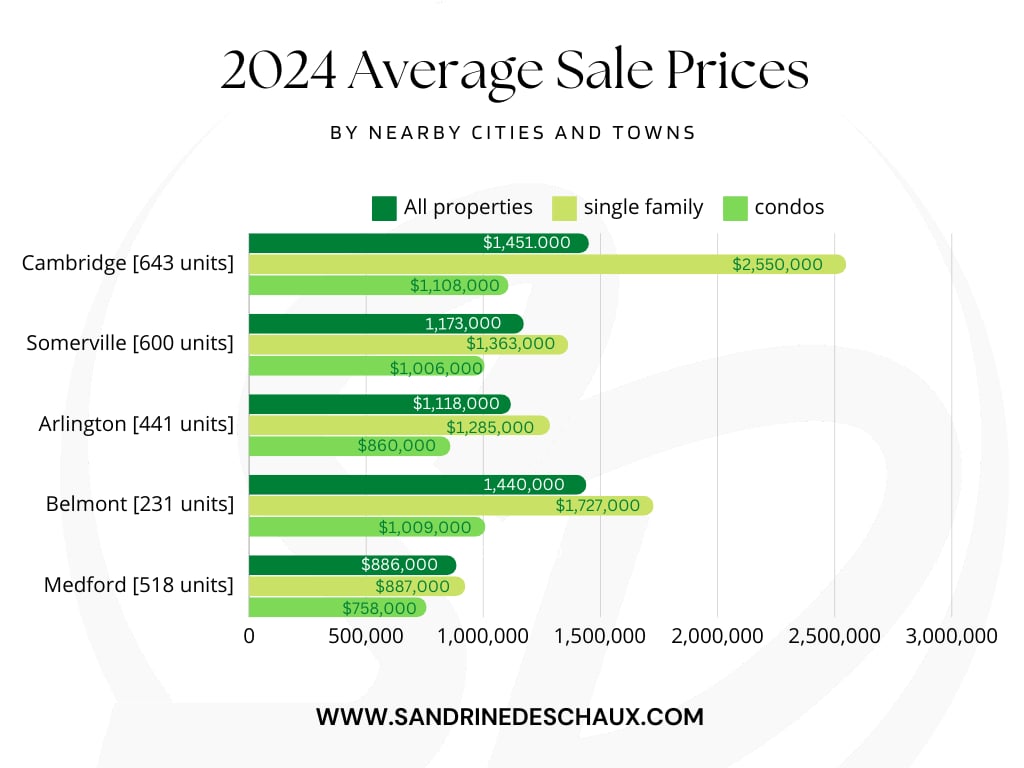

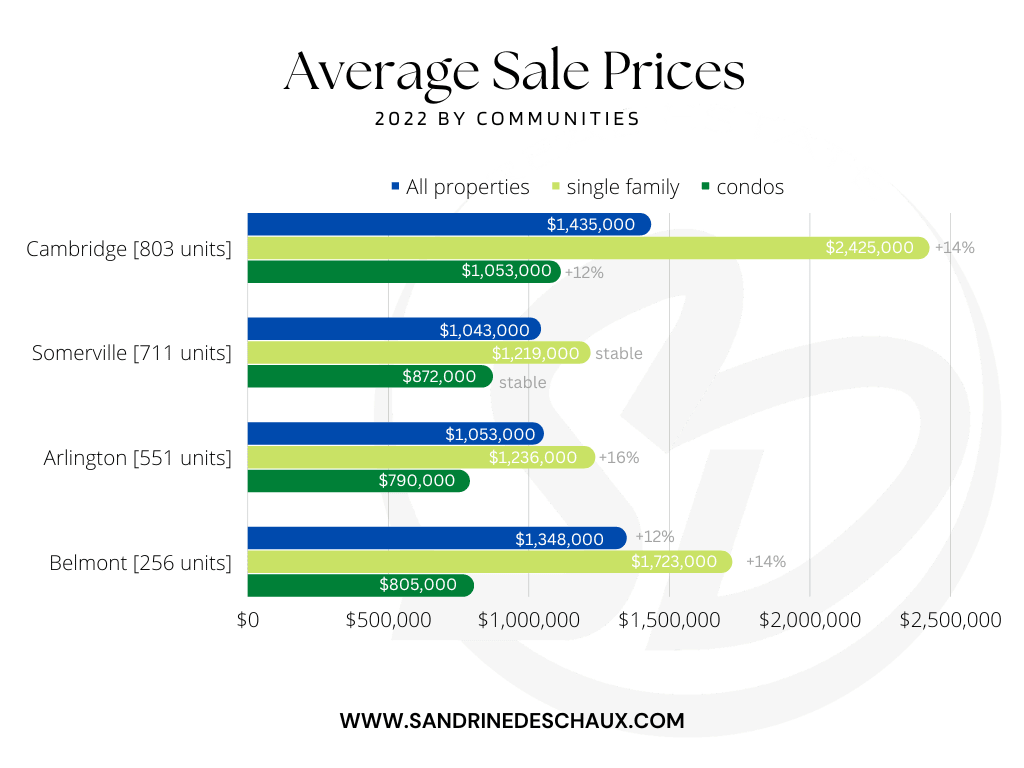

Conforming limits are county specific and update annually. Cambridge is in Middlesex County, which often sits on the higher end of limits for the Boston area. Because many Cambridge single-family prices are above the one-unit conforming threshold, buyers here frequently need jumbo financing.

Before you shop, confirm the current Middlesex County one-unit limit using the FHFA county lookup tool. Limits change every year, so check the latest number and verify it with your lender. You can use the FHFA conforming loan limits map to look up Middlesex County by state and county name.

- View the FHFA conforming loan limits lookup to confirm Middlesex County’s current limit: FHFA Conforming Loan Limits Map

When Cambridge buyers go jumbo

In Cambridge, you are most likely to cross into jumbo territory if you are purchasing:

- Larger single-family homes or high-end renovations.

- Luxury townhomes or newly built attached homes.

- Condominium units in premium communities with higher sale prices.

Local competition also plays a role. Nearby markets like Arlington, Somerville, Winchester, Newton, and Belmont influence buyer demand and pricing pressure. When multiple offers push the contract price higher, your loan amount may exceed the conforming threshold and move into jumbo territory.

What lenders look for on jumbo loans

Jumbo underwriting is more detailed than for conforming loans. Expect closer scrutiny and stronger borrower requirements. While programs vary by lender, here are common expectations:

Credit score

Most conventional jumbo products aim for 700 to 760 or higher for best pricing. Some portfolio lenders offer flexibility for lower scores, but expect higher rates or extra conditions.

Down payment and LTV

A 20 percent down payment, or 80 percent loan-to-value, is a common baseline. With top-tier credit, low debt, and strong reserves, you may see 10 to 15 percent down options. For condos, second homes, or investment properties, down payment requirements are often higher, commonly 25 to 30 percent.

Reserves

Lenders typically want to see 6 to 12 months of reserves after closing. Reserves are the total of principal, interest, taxes, and insurance, known as PITI. For very large loans, second homes, or higher debt-to-income scenarios, lenders may require more than 12 months.

Debt-to-income ratio

Jumbo loans usually target a lower DTI than conforming loans. Many lenders prefer 43 percent or less. Some may allow up to roughly 50 percent when you have strong compensating factors like high credit scores and large reserves.

Income and documentation

Plan for full documentation. Lenders will review W-2s, tax returns, and pay stubs. If you are self-employed, expect to provide business returns and detailed cash flow. Underwriters look for stable, recurring income and will question large deposits or nonrecurring income sources.

Past credit events and seasoning

If you have a prior bankruptcy or foreclosure, jumbo programs often require longer seasoning periods than conforming loans. Ask potential lenders about their specific timelines.

Mortgage insurance

Standard private mortgage insurance is designed for conforming loans and is not typical for jumbos. Lenders may use piggyback seconds, lender-paid solutions, or simply require a larger down payment instead of PMI.

Rates, products, and how to choose

Jumbo rates are driven by your credit, down payment, reserves, property type, and whether the lender sells the loan or holds it in portfolio. Because jumbos do not go into the same agency pools as conforming loans, rates are often a bit higher. The gap can be small, like a few basis points, or larger depending on market conditions and lender appetite.

You will see a range of products:

- Conforming loans: Best pricing and widest availability, but only up to the county limit.

- High-balance agency-eligible loans: In some high-cost counties, there are higher conforming limits that still allow agency delivery. Check the county lookup and discuss with your lender.

- Jumbo loans: Fixed or adjustable rate options from banks, mortgage companies, and credit unions.

- Portfolio and super-jumbo programs: Held by the lender, sometimes with more flexible underwriting for well-qualified borrowers.

- Non-QM or bank-statement programs: Used for unique income profiles, usually at higher rates and with stricter reserve requirements.

Comparing offers from multiple jumbo-experienced lenders can reveal meaningful differences in rates, closing timelines, and underwriting flexibility.

Appraisals and valuation in Cambridge

Most jumbo loans require a full traditional appraisal. In a competitive market, appraiser availability can affect timing. For high loan amounts or unique properties, some lenders ask for a second appraisal or a desk review.

Also consider appraisal gap risk. If your accepted offer is higher than the appraised value, your lender will base the loan amount on the appraisal, not the purchase price. You would need to cover the difference in cash or renegotiate with the seller. Talk with your agent about appraisal strategies before you write an offer.

Condo and townhome considerations

Condo eligibility matters more with jumbo financing. Lenders review the project’s financials, owner-occupancy rates, reserve levels, and any litigation. If a project shows high investor concentration or active legal issues, financing can be difficult.

If you are targeting a luxury condo or townhome, request the condo questionnaire, budget, and key documents early. Confirm project status with your lender before you make an offer so you understand any added down payment needs or reserve requirements.

Budgeting for taxes, insurance, and HOAs

Your monthly affordability and reserve requirements depend on more than principal and interest. In Arlington, property taxes, homeowners insurance, and any HOA fees count toward your DTI. If the home is in a flood zone, flood insurance may also apply. Surface these costs early with your lender so your pre-approval reflects the full picture.

Build a winning offer with jumbo financing

To compete well on a jumbo purchase in Arlington, focus on strength and certainty.

- Get a full pre-approval, not a pre-qualification. A strong pre-approval includes a credit pull, verified assets, and documented income, which helps sellers trust your offer.

- Demonstrate cash strength. Larger earnest deposits, clear proof of funds for your down payment, and documented reserves can reduce seller hesitation.

- Consider ways to access down payment funds. If your equity is tied up in a current home, ask your lender about bridge options or other strategies to align timelines.

- Use offer terms that reduce seller risk. Shorter financing and appraisal contingencies can stand out, but weigh the risks before tightening timelines. If you are considering an appraisal gap commitment, set a clear dollar cap that matches your cash position.

- Work with local expertise. Choose a lender that uses appraisers familiar with Arlington neighborhoods to reduce surprises. Your agent can package strong local comparable sales with your offer to support value.

- Be proactive on condos and townhomes. Confirm project eligibility and any lender overlays before you submit an offer.

How to check the limit and plan next steps

Follow these steps to confirm whether your loan is jumbo and to build a smooth path to closing:

- Look up Middlesex County’s current one-unit conforming limit using the FHFA Conforming Loan Limits Map. Note that limits change annually.

- Match the property type. Check whether you need the one-unit limit or a 2 to 4 unit limit if applicable.

- Talk with a jumbo-experienced lender. Share your income documents and asset statements to get a complete pre-approval that reflects taxes, insurance, and any HOA fees.

- Align your strategy with your agent. Discuss appraisal risks, condo project eligibility if relevant, and offer terms that fit your comfort level and cash reserves.

- Stay flexible as rates move. Ask for updated quotes and timing from more than one lender. Portfolio appetite can shift, which may improve your pricing or terms.

Buying in Arlington with jumbo financing is very doable when you prepare early and present a strong, clear file. If you want a local strategy for the neighborhoods you are targeting, connect with an advisor who navigates these nuances every week.

Ready to talk through jumbo strategies, appraisal risk, and offer terms for Arlington homes you love? Schedule a Consultation with Sandrine Deschaux to map your best path to a confident purchase.

FAQs

How to tell if my Cambridge loan is jumbo

- If your loan amount exceeds the current Middlesex County conforming limit for your property type, it is a jumbo. Verify the limit with the FHFA lookup and your lender.

Typical credit scores for a jumbo mortgage

- Many jumbo lenders look for 700 to 760 or higher for best pricing, with some portfolio options for lower scores at higher rates or with more conditions.

Minimum down payment for jumbo loans in Cambridge

- A 20 percent down payment is common. Some lenders offer 10 to 15 percent down for top-tier borrowers, usually with higher rates and stronger reserve requirements.

Do jumbo loans need two appraisals in Cambridge

- Not always. Lenders may order a second appraisal or a review for higher loan amounts or unique properties, especially when comparable sales are limited.

Are condos harder to finance with a jumbo

- Yes. Jumbo lenders apply stricter condo project reviews, including owner-occupancy, reserves, and litigation checks. Confirm project eligibility early with your lender.