Winning a home in Cambridge often comes down to speed and certainty. You may hear two terms at the start of your search that sound similar but carry very different weight with sellers: pre-qualification and pre-approval. If you are trying to compete for a great condo or single-family, knowing the difference can shape your strategy and your success. This guide shows you what each means, why pre-approval matters in Cambridge, and how to prepare so you can write a confident offer. Let’s dive in.

Pre-qualification vs. pre-approval: the short version

- Pre-qualification is an estimate based on information you share with a lender. It may not include document checks or a hard credit pull, so it is helpful for early budget planning but weak in negotiations. Investopedia explains the differences between pre-qualification and pre-approval.

- Pre-approval is a lender-verified, conditional commitment. It typically includes a full application, document review, and a hard credit pull, and results in a letter stating a loan amount subject to conditions like appraisal. It is not final approval, but it is far stronger than pre-qualification. Learn more about what a mortgage pre-approval includes.

Why pre-approval matters in Cambridge

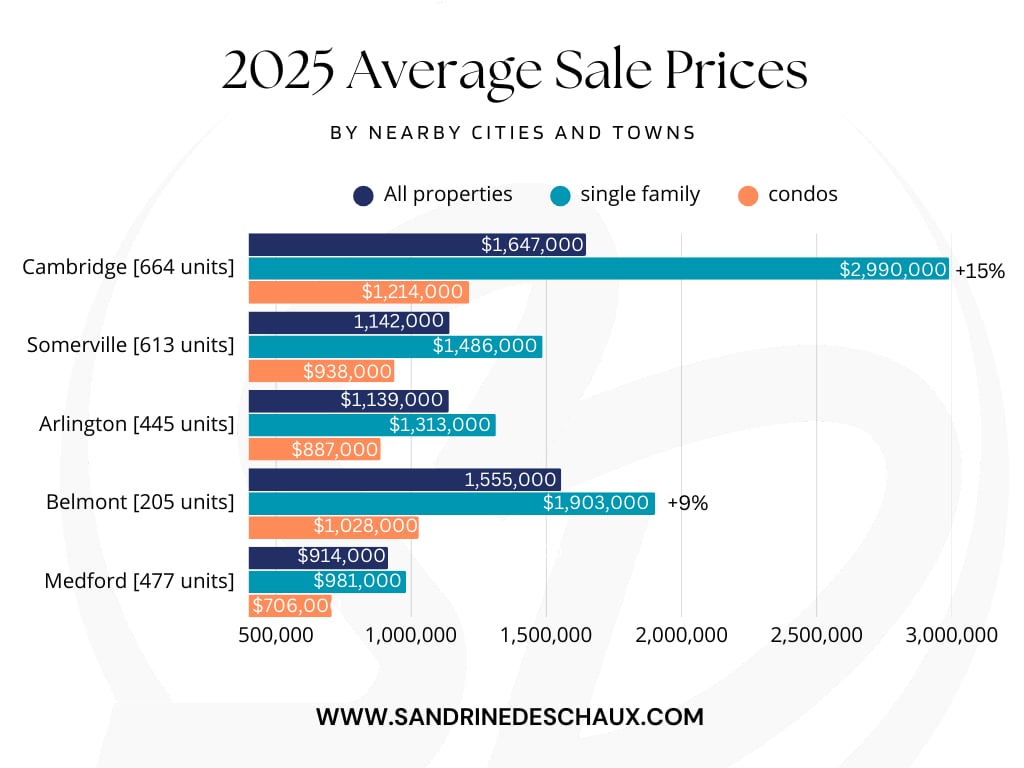

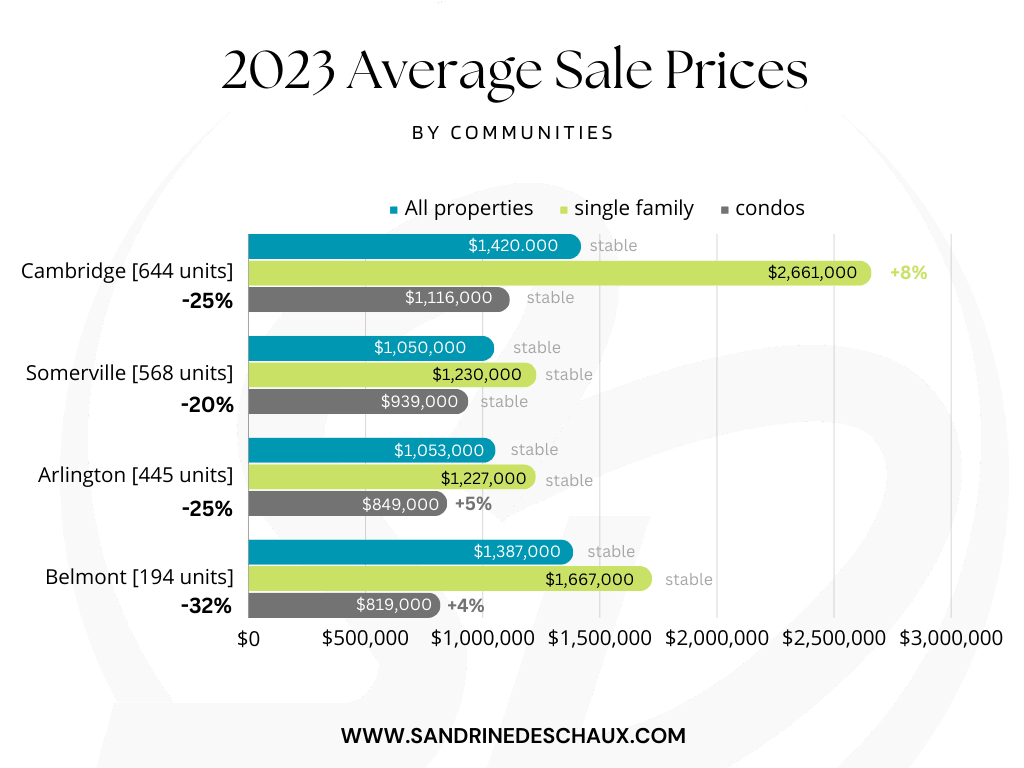

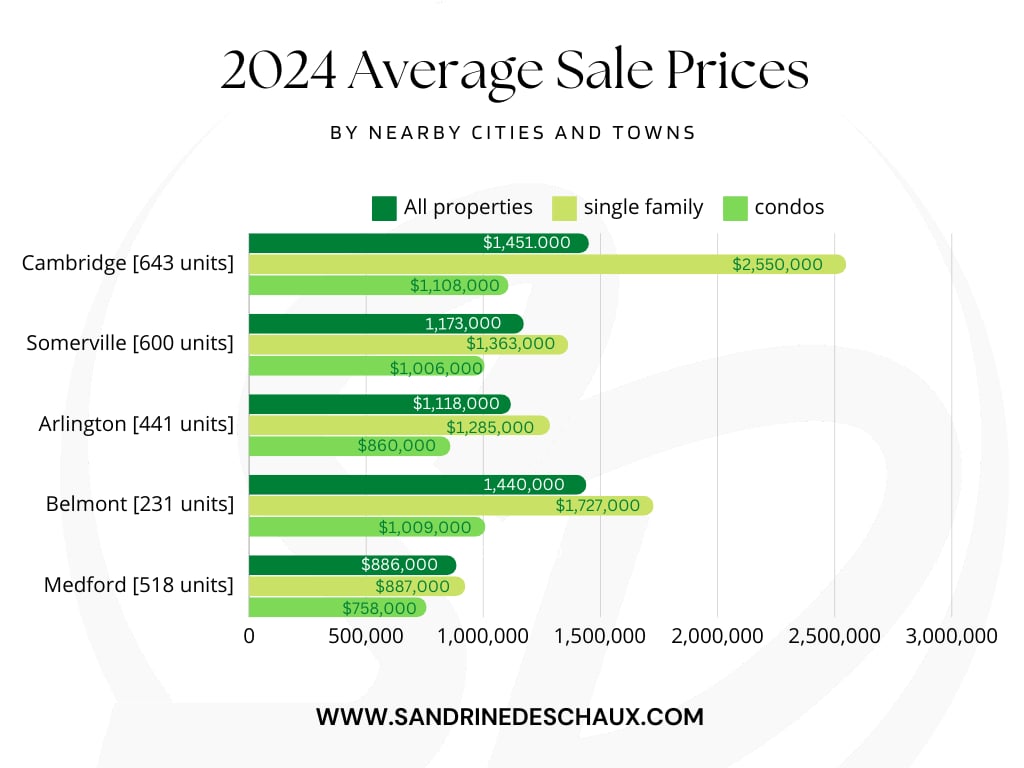

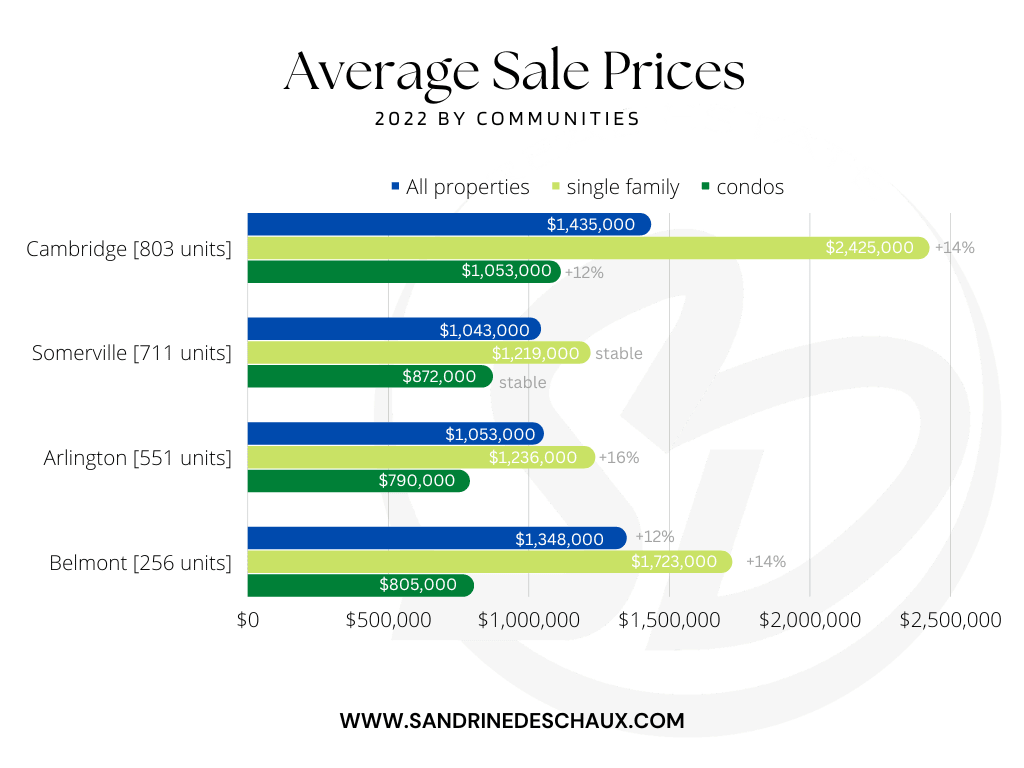

Cambridge is a very competitive market with many homes attracting multiple offers and seven-figure price points. In this environment, sellers want proof that you can perform. A current pre-approval tells the listing side you have already cleared key lender checks, which lowers the risk of a financing delay.

Regional price trends also add pressure. Greater Boston’s single-family median recently hit about one million dollars, which affects affordability and competition across the inner suburbs. See the regional context from Axios on Greater Boston pricing.

How pre-approval works

Pre-approval follows a defined process and typically results in a letter that is valid for a limited time.

Steps to get pre-approved

- Apply with a lender or mortgage broker, often using the Uniform Residential Loan Application. You can review the application format on HUD’s site.

- The lender pulls a hard credit report, which can cause a small, temporary dip in your score. Read more about how pre-approval works and credit pulls.

- You submit documents so the lender can verify income, assets, and employment. This is where most timelines speed up or slow down based on your completeness. See a common mortgage document checklist.

- You receive a written pre-approval letter with a conditional loan amount and terms. Letters often remain valid for about 60 to 90 days and may need refreshing if they expire.

What lenders verify

Lenders typically review your pay stubs, W-2s or tax returns, bank and investment statements, debt obligations, and employment. They also calculate your debt-to-income ratio and confirm you have sufficient funds for your down payment and reserves. Some may request letters for large deposits or gift funds as part of verification.

Timeline and how to move fast

Pre-approval can take a few days to two weeks. The quickest path is to gather your documents early and respond to lender requests promptly. Keep your letter current because most expire in 60 to 90 days. If it expires, expect to refresh your credit check and provide updated statements.

Document checklist to get ready

Having your documents ready before you tour homes helps you act fast when the right property hits the market.

- Government ID and Social Security number

- Recent pay stubs and last 1 to 2 years of W-2s; tax returns if self-employed

- Bank and asset statements for the past 2 to 3 months

- Proof of additional income, if applicable

- Employment verification details and contacts

- Explanations for large deposits and gift letters, if applicable

For another reference, review this lender home loan document checklist and the common mortgage document list.

Pair pre-approval with Cambridge assistance

You can strengthen affordability by combining a lender pre-approval with local and state programs, when eligible.

- Cambridge HomeBridge. The City’s HomeBridge program provides financial assistance to eligible first-time buyers purchasing on the open market in exchange for an affordable housing restriction. It requires a separate City application, CHAPA-certified education, and a conventional fixed-rate mortgage. Approved applicants receive a City pre-approval that can be paired with a lender letter. Review details on Cambridge’s HomeBridge page.

- Cambridge Down Payment Assistance. The City also offers down payment assistance for eligible first-time buyers, typically as a forgivable or subordinated loan with published limits. Learn more on the City’s homebuyer resources page.

- MassHousing DPA. MassHousing expanded its statewide down payment assistance in 2025, offering income-tiered assistance up to 25,000 to 30,000 dollars when used with a MassHousing mortgage and an approved lender. See the MassHousing announcement.

Programs have their own eligibility rules, documentation, and in the case of HomeBridge, resale covenants. Review requirements closely before you apply.

Use your letter to strengthen offers

When you write in Cambridge, plan to include a current pre-approval letter that names your loan amount and lender contact. Add a proof-of-funds statement for your down payment. If you are using City or state assistance, include your program pre-approval or eligibility confirmation as available.

You can make your offer more persuasive by working with a lender who understands Cambridge programs like HomeBridge or MassHousing. Keep your documents current and your lender reachable so the listing agent can quickly verify your strength.

Next steps for Cambridge buyers

- Take a CHAPA-certified first-time buyer class if you are eligible and plan to use City programs, then gather your financial documents.

- Get pre-approved with a reputable lender and ask how they handle credit pulls and rate locks.

- If you may qualify for HomeBridge or City down payment assistance, begin the City application in parallel with lender pre-approval. Start here: Cambridge homebuyer resources.

- Explore whether MassHousing DPA applies to you and which lenders are approved. Read the MassHousing DPA overview.

- Refresh your pre-approval if it nears expiration, then be ready to write promptly when the right home appears.

Ready to compete with confidence in Cambridge? Partner with a local advisor who knows the micro-markets, programs, and offer strategies that move the needle. If you want one-on-one guidance or a referral to trusted lenders, reach out to Sandrine Deschaux.

FAQs

What is the difference between mortgage pre-qualification and pre-approval?

- Pre-qualification is an estimate based on self-reported info, while pre-approval is a lender-verified conditional commitment with a hard credit pull and document review. See Investopedia’s explainer.

Why does pre-approval matter in competitive Cambridge home sales?

- Sellers favor offers with verified financing because they are less likely to fall through. Pre-approval shows you completed key checks and can move quickly at Cambridge price points.

Will getting pre-approved lower my mortgage interest rate?

- Pre-approval does not guarantee a specific rate. Final pricing depends on your credit, loan product, and market conditions, and some lenders only lock rates at certain stages. Learn more about pre-approval and rates.

Does a pre-approval hurt my credit score?

- A hard credit inquiry for pre-approval can cause a small, temporary dip. Rate-shopping inquiries for the same mortgage type within a short window are often treated as a single inquiry by scoring models.

How long does a mortgage pre-approval last for Cambridge buyers?

- Many letters are valid for 60 to 90 days. If yours expires, expect to refresh your credit check and provide updated documents before writing offers again.

Can a lender withdraw my pre-approval after I make an offer?

- Yes, if your finances change significantly, your credit shifts, or the property has appraisal or title issues. Pre-approval is conditional, not final approval.

Are there Cambridge programs I can combine with lender pre-approval?

- Yes. Eligible buyers can apply for the City’s HomeBridge and down payment assistance, and some may qualify for MassHousing DPA. Start with Cambridge’s homebuyer resources and the MassHousing update.

How can I spot misleading mortgage “pre-approval” ads?

- The CFPB cautions consumers about potentially deceptive ads. Review lender offers carefully and see this CFPB advisory for red flags to avoid.