Looking at a two or three family in Somerville and wondering if the numbers pencil? You are not alone. In a market shaped by top employers, transit access and limited land, cash flow can feel tight while appreciation looks compelling. In this guide, you will see how rents really work, what returns to expect, how to underwrite deals, and where value add strategies move the needle. Let’s dive in.

Why Somerville draws investors

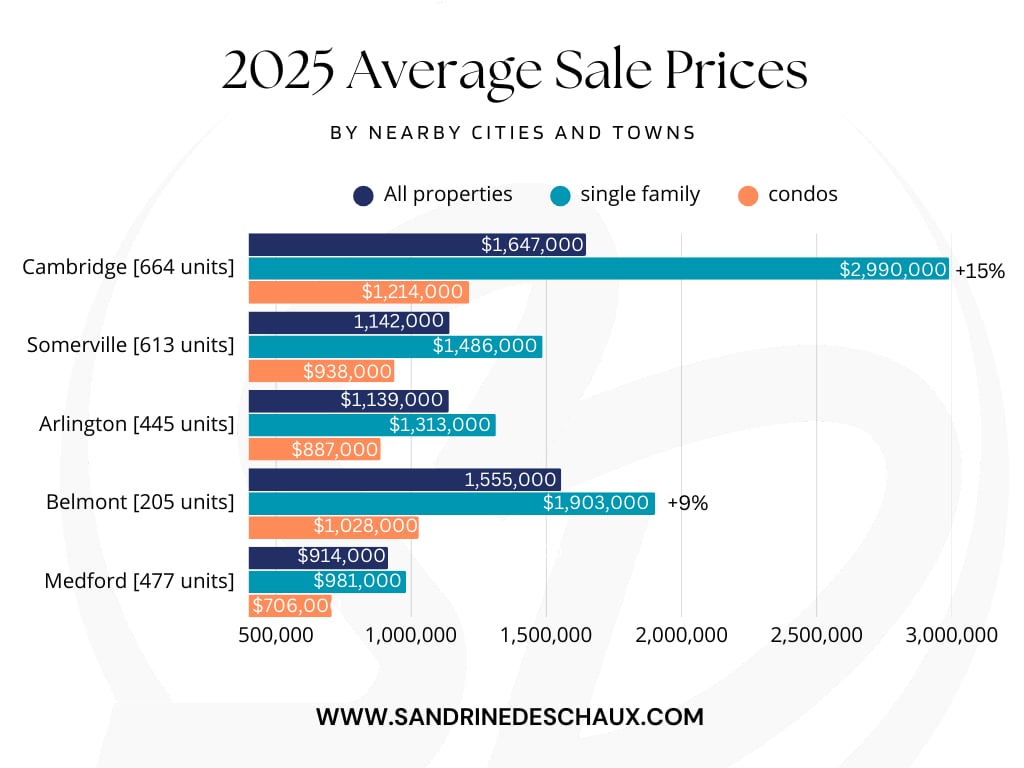

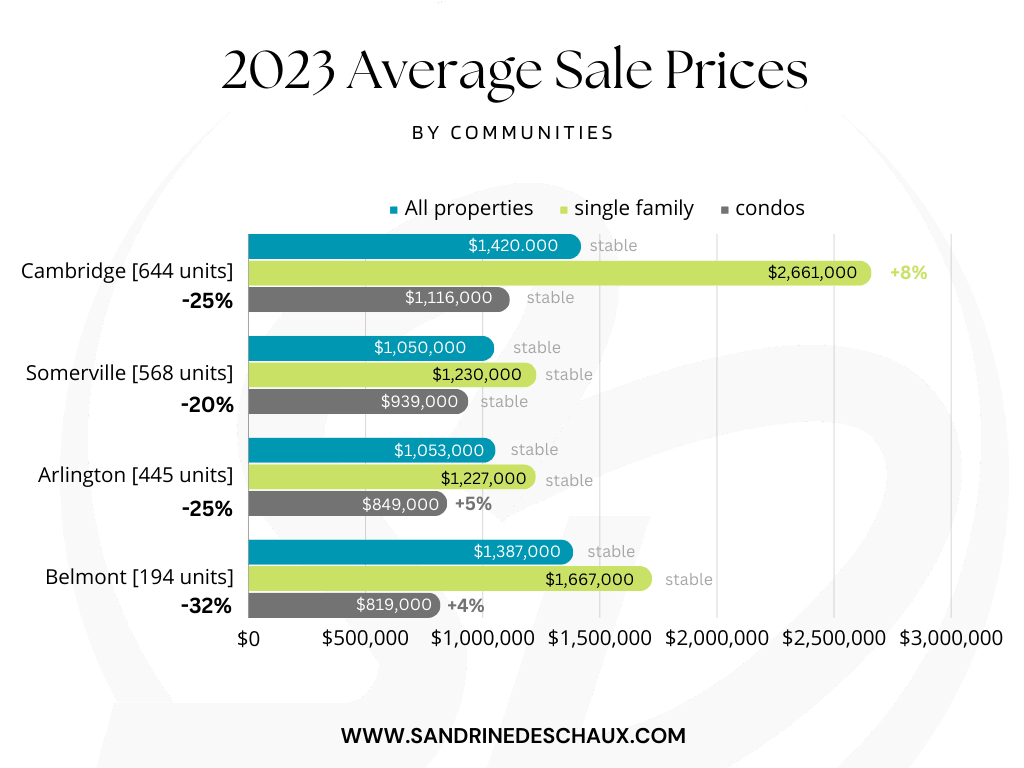

Somerville sits in Boston’s inner ring with steady renter demand tied to Cambridge’s tech and biotech cluster, hospitals and universities. Multiple MBTA corridors, high walk and bike scores, and scarce developable land support strong rents and appreciation potential relative to many outer suburbs. Micro location is critical. Blocks near Davis, Porter, Union and Assembly often command premiums, while quieter streets can deliver stable occupancy and lower turnover. Recent appreciation has compressed cap rates, so today’s small multifamily often trades with lower cash yields unless you execute a value add plan or select higher yield pockets.

Rents: what sets the range

Unit type and condition

Most two and three families are older wood frame buildings with one unit per floor. Condition matters. Unrenovated kitchens and baths generally rent for less, while upgraded interiors with in unit laundry, modern systems and good finishes can command a meaningful premium. Expect a several hundred dollar gap per unit between dated spaces and well renovated apartments near key squares.

Micro location near transit

Apartments within a short walk of Davis, Porter, Union or Assembly typically rent at the high end for Somerville. Street level differences within a few hundred feet can shift rent and absorption. Proximity to commercial corridors and parks also helps with pricing and retention.

Amenities and utilities

In unit amenities like laundry, air conditioning and storage boost marketability. Utility setups matter too. Master metered buildings often carry higher owner paid expenses, while separated utilities can lower operating costs and support stronger net income.

Returns: yield versus appreciation

Small multifamily in Somerville is a tradeoff. Tight cap rates and today’s rate environment mean lower cash yields on stabilized, renovated assets in prime micro locations. Many investors lean on appreciation, operational improvements or targeted renovations to reach return goals. If you are buying for cash flow, be precise about unit quality, metering and expenses, or look for value add opportunities where you can move rents to market over time within tenant protection rules.

Underwrite with discipline

Revenue to model

- Scheduled rent by unit for current and market rates

- Other income from laundry, parking, storage, pet fees and utilities passed through

- Vacancy and collection loss using local assumptions, commonly 4 to 8 percent depending on unit quality and micro market

Expenses to model

- Property taxes based on the assessor’s value and the current rate

- Insurance for building and liability

- Utilities for water and sewer, common area electric, and any owner paid heat or hot water

- Repairs and maintenance for older systems plus seasonal services

- Capital reserves for big ticket items like roof, boilers, windows and kitchens

- Management, whether owner operated or third party at roughly 6 to 10 percent of effective gross income

- Administrative, legal and accounting

- Marketing and turnover costs between leases

Conservative ranges to use

- Vacancy and collection loss: 4 to 8 percent

- Management fee: 6 to 10 percent of effective gross income

- Repairs and maintenance: often 5 to 10 percent of effective gross income, higher for older buildings

- Capital reserves: commonly budgeted separately, often 250 to 600 dollars per unit per month for older properties

- Insurance: wide variance, frequently modeled as a percentage of property value

- Utilities: review actual bills to set realistic assumptions

Core metrics you need

- Effective Gross Income (EGI) equals potential gross rent minus vacancy plus other income

- Net Operating Income (NOI) equals EGI minus operating expenses, excluding debt service

- Cap rate equals NOI divided by purchase price

- Cash on cash return equals annual cash flow after debt service divided by equity invested

- Gross Rent Multiplier (GRM) equals purchase price divided by gross scheduled rent

Simple pro forma template

- Potential Gross Rent: sum of all unit rents at market

- Less Vacancy and Collection Loss: apply 4 to 8 percent

- Plus Other Income: laundry, parking, storage and fees

- Equals Effective Gross Income (EGI)

- Less Operating Expenses: taxes, insurance, utilities, repairs, management, admin

- Less Capital Reserves: set aside for systems and major components

- Equals Net Operating Income (NOI)

- Less Debt Service: based on your loan terms and down payment

- Equals Annual Cash Flow and Cash on Cash Return

Stress test your model. Small shifts in vacancy, management costs, capital needs or interest rate can materially change cash flow in a low cap rate environment.

Financing paths to consider

Local banks and portfolio lenders actively finance 2 to 4 unit properties. Conventional and agency options exist for this size segment, with FHA available for owner occupants who meet requirements. Owner occupants often access better terms and lower down payments by living in one unit. Non owner investors should plan for roughly 20 to 25 percent down and lender debt service coverage tests. Model refinance and exit scenarios with potential prepayment penalties and a conservative exit cap rate.

Value add that moves the needle

Interior upgrades

Renovating kitchens and baths, improving lighting and flooring, and adding in unit laundry tend to be the most straightforward path to rent uplift. These changes also reduce turnover by improving livability.

Systems and metering

Upgrading heating systems, installing individual hot water solutions and separating meters can lower ongoing owner expenses. Over time, operational savings and clearer utility responsibility support stronger net income.

Repositioning rents

Bringing below market units to market on turnover is a common strategy. Plan a staged approach that aligns with tenant protections, proper notice and local rental registration requirements.

Bigger moves need approvals

Reconfiguring units, adding units or legalizing basement and attic spaces requires zoning and building code compliance. Somerville’s zoning, historic districts and permitting processes can add time and complexity. Short term rentals and accessory dwelling units may be limited, so verify rules before underwriting alternative income.

Due diligence checklist

- Verify legal unit count and occupancy on the certificate of occupancy

- Review leases, rent roll, security deposit records and rent receipts for 12 to 24 months

- Pull municipal records from Somerville Inspectional Services and the Assessing Office for permits, violations and tax history

- Inspect structure, roof, foundation, moisture, heating systems, hot water, electrical capacity and any older wiring

- Check for lead paint risks in pre 1978 buildings and other health or safety issues

- Collect 12 to 24 months of utility bills for gas, electric and water or sewer

- Review insurance history and coverage

- Order title work and check for easements, encroachments and parking rights

- Confirm zoning, potential for additional units and historic district status

- Evaluate environmental and flood risk using official maps and any local history

- Build a pro forma with pessimistic, base and optimistic cases to see how the deal performs across scenarios

Two paths, two outcomes

A fully renovated two family near Davis or Union may command top of market rents and experience low turnover. The purchase price often implies a lower cap rate, so cash yield can feel thin without leverage optimization or additional income streams. In contrast, an unrenovated three family in a more residential pocket may trade at a lower price with higher near term upside through renovations. That path requires capital, time and careful navigation of permitting and tenant protections, but it can shift net income once work is complete.

Put local expertise to work

Somerville’s small multifamily market is block by block and building by building. Two similar looking three families can produce very different outcomes based on transit access, systems and policy constraints. If you want a clear read on rents, expenses and value add scope before you write an offer, let’s talk. Connect with Sandrine Deschaux to get micro market insight, underwriting guidance and a plan tailored to your goals.

FAQs

What drives rent premiums in Somerville?

- Proximity to Davis, Porter, Union and Assembly, renovated interiors, in unit amenities and walkability generally push rents to the high end, while dated finishes and master metered utilities tend to price lower.

How much vacancy should I underwrite for small multifamily?

- Many investors model 4 to 8 percent for vacancy and collection loss in Somerville, adjusting based on unit quality, micro location and management approach.

What are typical management and reserve assumptions?

- Third party management often runs 6 to 10 percent of effective gross income. For older buildings, capital reserves are commonly set at 250 to 600 dollars per unit per month.

Which financing options are common for 2 to 4 units?

- Portfolio and local banks are active, with conventional and agency products available. Owner occupants may access FHA and lower down payments, while investors often plan 20 to 25 percent down and meet DSCR guidelines.

What due diligence is unique to Somerville?

- Confirm rental registration, permits and code status with Somerville Inspectional Services, verify legal unit count, and check zoning or historic overlays before assuming any unit reconfiguration or additions.