Thinking about buying in Cambridge but torn between a lock-and-leave condo and the privacy of a single-family home? With prices, fees and daily rhythms that feel worlds apart, the right choice is not always obvious. You want a home that fits your lifestyle and a monthly number that makes sense. In this guide, you’ll compare costs line by line, see how neighborhoods differ and learn what to check in condo associations and financing so you can buy with confidence. Let’s dive in.

Cambridge prices at a glance

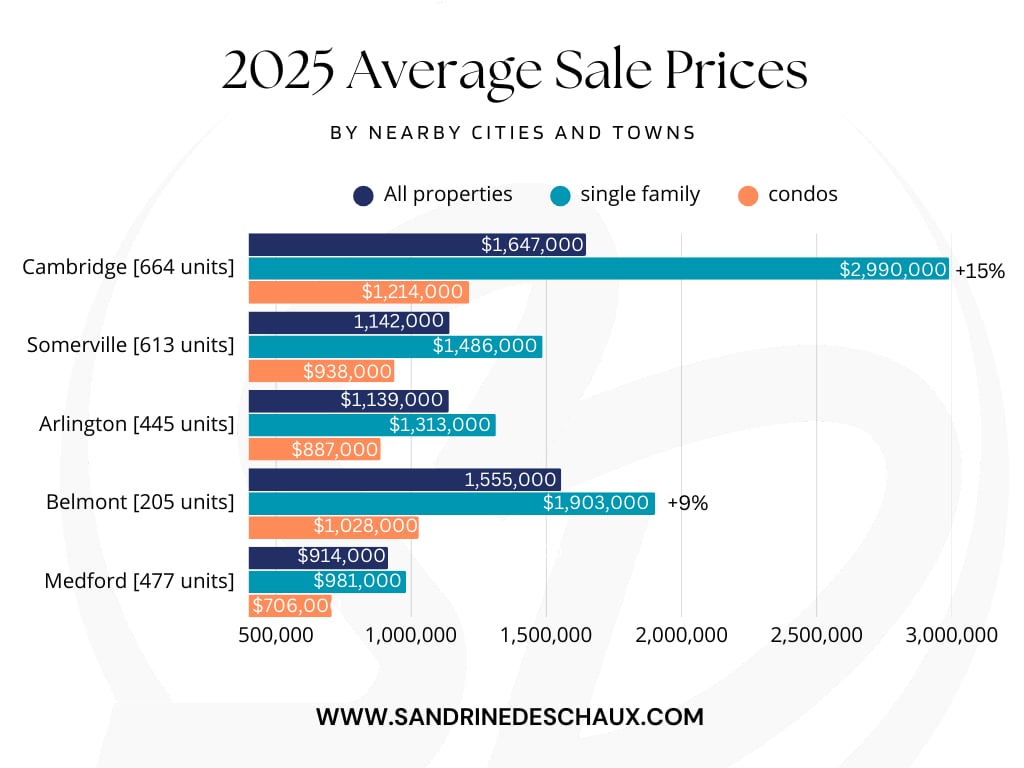

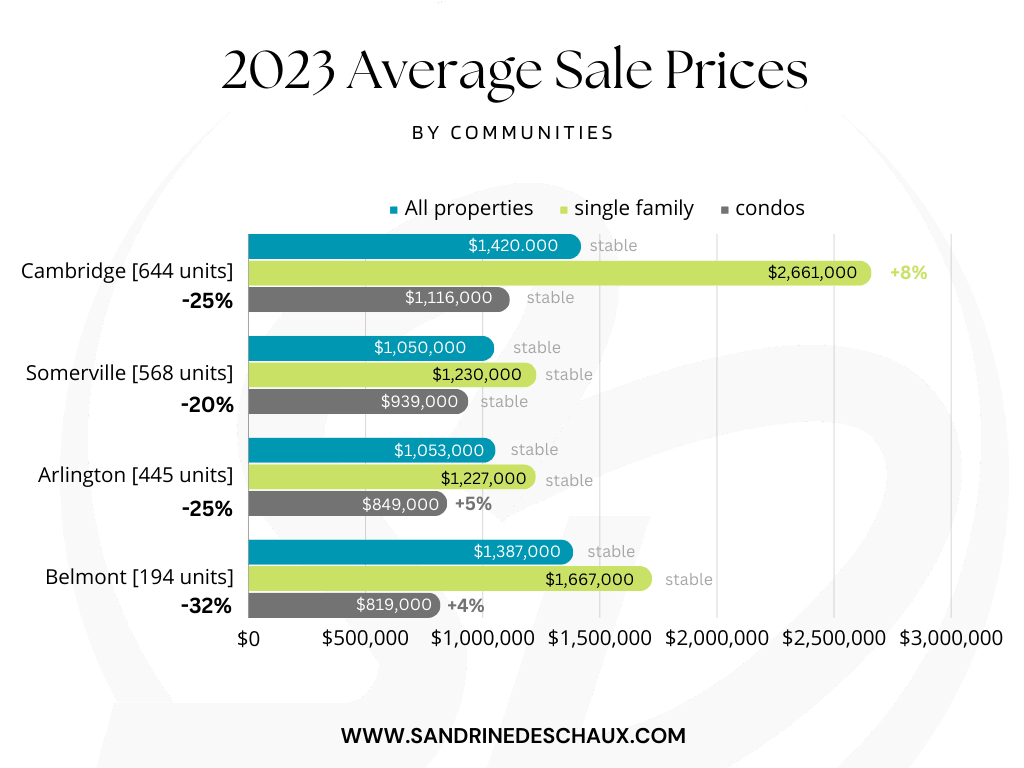

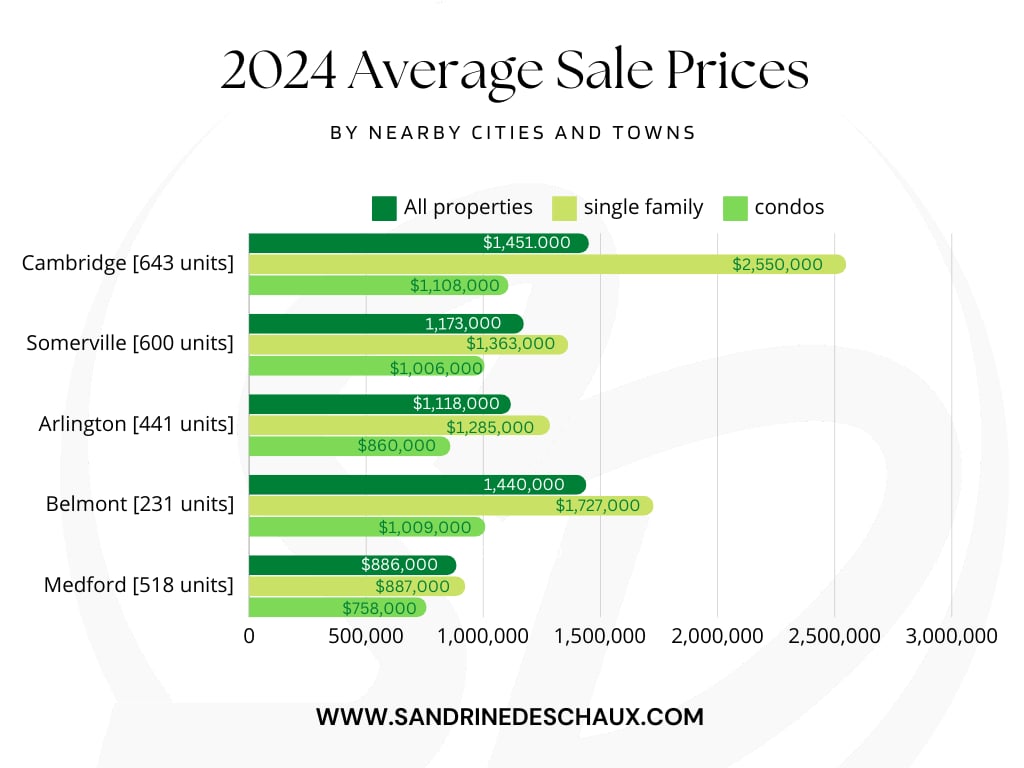

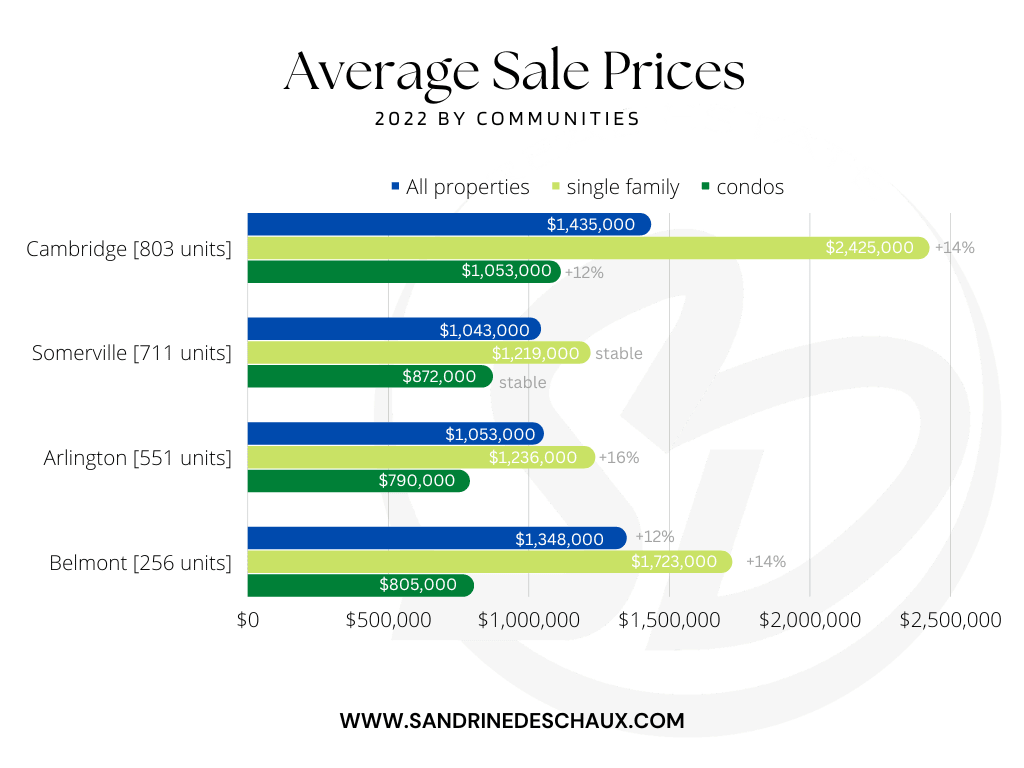

Citywide medians vary by source and timing. As of Feb 2026, Redfin reported a Cambridge median sale price around $940,000. Local MLS summaries for year-end 2025 showed a large gap by property type, with condo medians near $975,000 and single-family medians around $2,505,000. Different trackers use different windows, so always note the source and date when you compare.

West Cambridge

West Cambridge is one of the city’s highest-value pockets with many historic homes, larger lots and private yards. Median prices here often land in the high seven figures. Inventory is limited and hold times tend to be long, which supports values over time.

Mid-Cambridge

Mid-Cambridge mixes condos and smaller single-family homes near Harvard and Central Square. Redfin reported a neighborhood median around $930,000 in Feb 2026. It suits buyers who want a residential feel with strong walkability and access to daily amenities.

Cambridgeport

Cambridgeport sits near the Charles with many condos and conversions. Neighborhood medians have recently hovered in the low seven figures. It attracts buyers who like river access and quick commutes to Kendall and MIT.

Data note: Medians differ across services and timeframes. Use live sources and date each stat. For clear neighborhood boundaries, see the City’s Community Development Department neighborhood map.

Cost of ownership, line by line

When you compare a Cambridge condo with a single-family home, add every cost that hits your monthly budget.

- Mortgage principal and interest (from your lender)

- Property taxes

- HOA/condo dues (if condo)

- Homeowner or condo insurance

- Maintenance reserve

- Utilities

- Parking

Property taxes (FY26)

Cambridge’s FY26 residential property tax rate is $6.67 per $1,000 of assessed value. On an assessed value of $1,000,000, the annual tax is about $6,670, or roughly $556 per month. The City explains the rate and method in its Property Tax Rate Executive Summary. You can look up assessed values and estimated bills in the City’s Assessing Department to model a specific address.

Practical tip: Cambridge offers a residential exemption for qualifying owners. Confirm eligibility with the City when you budget.

HOA dues and special assessments

Condo dues in Cambridge range widely. Smaller 2–4 unit buildings can have modest fees, while amenity buildings with concierge, gym or garage often exceed $1,000 per month. Boards may levy special assessments when reserves are not enough for big projects. That risk is the key tradeoff for condo owners in older or amenity-rich buildings. Recent coverage of ownership “hidden costs” across Greater Boston underscores why you should plan beyond the mortgage payment and dues. See the Boston Globe’s analysis of taxes, insurance and maintenance add-ons in the region’s housing costs (Greater Boston hidden cost overview).

Reserves, law and risk

Massachusetts requires condominium associations to keep an “adequate replacement reserve fund” and segregate it from operating funds. The statute does not set a fixed percentage, so reserve studies and visible balances are what lenders and buyers use to gauge risk. Strong reserves can reduce the chance of large special assessments. You can read a practical overview of state reserve requirements in this Massachusetts condo reserve guide and a legal discussion of Chapter 183A §10(i) here: condo association reserve funding.

Insurance and maintenance

Insurance and upkeep matter in Cambridge’s older housing stock and New England weather. The Boston Globe’s recent review of national and Greater Boston data highlights that maintenance, taxes and insurance can add materially to monthly costs. A common planning rule is to reserve about 1 percent of a home’s value per year for maintenance, adjusting upward for age and weather exposure. For condos, part of your upkeep is handled through association dues, but set aside a personal reserve for interior systems and finishes.

Parking and vehicle costs

Deeded or assigned parking is a major differentiator. Many Cambridge condos, especially older conversions, do not include a deeded space. If a property lacks on-site parking, plan for a resident street permit and, if needed, a monthly garage or lot. Review City rules for permits and eligibility on the Traffic, Parking & Transportation page.

A quick monthly comparison

Below is a simple side-by-side using common Cambridge scenarios. Replace the inputs to match the property you’re considering.

| Line item | Example condo ($1.20M) | Example single-family ($2.40M) |

|---|---|---|

| Mortgage P&I | From lender | From lender |

| Property tax (FY26 $6.67 per $1,000) | ~$8,004/yr ≈ $667/mo | ~$16,008/yr ≈ $1,334/mo |

| HOA/condo dues | ~$900/mo (varies) | $0 |

| Insurance | Estimate with insurer | Estimate with insurer |

| Maintenance reserve (1% rule) | ~$12,000/yr ≈ $1,000/mo | ~$24,000/yr ≈ $2,000/mo |

| Parking | If rented, add monthly rate | If rented, add monthly rate |

| Subtotal before mortgage & insurance | ~$2,567/mo | ~$3,334/mo |

Notes:

- Assessed value can differ from purchase price. Use the City’s assessing tools to refine the tax estimate by address.

- HOA dues and special assessments can change based on building reserves and projects. Review the budget and minutes closely.

- Maintenance is a planning reserve. Actual outlays vary by age, systems and exposure.

Lifestyle tradeoffs to consider

Why choose a condo

- Lower exterior maintenance since the HOA handles common areas and building systems.

- Amenities and security are common in high-end buildings near Kendall and East Cambridge, including concierge, package rooms and gyms.

- Lock-and-leave convenience for frequent travel or a second home.

- Proximity to restaurants, transit and employers if you value location over private outdoor space.

Where a condo can fall short

- Monthly dues and special assessment risk. Rules may limit renovations, pets or rentals.

- Less privacy and limited private outdoor space unless a unit has a terrace or deeded yard.

- Financing can narrow if the project is not eligible with major lenders. See “Financing and warrantability” below.

Why choose a single-family home

- More privacy, control and yard space. West Cambridge is the prime pocket for larger lots and tree-lined streets.

- No HOA dues and more control over the timing and scale of renovations.

Where a single-family can stretch you

- You are responsible for all exterior systems and grounds, so plan a larger maintenance budget.

- Inventory in Cambridge’s single-family segment is tight and competition is concentrated at the high end.

Financing, warrantability and resale

Project warrantability and loan options

Condo projects must meet specific standards for most conventional loans. Lenders and the major agencies review items like reserves, insurance, investor concentration and whether there are critical repairs. If a building fails a project review, the buyer pool can shrink to cash or portfolio loans. Ask your lender early about a building’s status and documentation. For a helpful overview of project reviews and what lenders look for, see this condo project review guide.

What to review in HOA documents

- Current budget and balance sheet with an eye on reserve strength.

- Board meeting minutes for the past 12 months to spot deferred maintenance or litigation.

- Master insurance declarations, including deductible size and replacement cost coverage.

- Recent and pending special assessments, plus any engineering reports for building systems.

Resale behavior and liquidity

In Cambridge, single-family homes in premium pockets trade in a smaller, high-price market with fewer listings. Condos near Harvard, Central and Kendall tend to draw a larger buyer pool, which can support faster resale but also reacts more quickly to interest rate and rent shifts. If you lean toward a condo, favor well-managed buildings with strong reserves to preserve your buyer pool.

Which fits your life? Three buyer profiles

The yard and privacy seeker

You want a quiet retreat, outdoor space and control over renovations. You value long-term holding and are comfortable with larger maintenance planning. Focus on West Cambridge and selected pockets that offer on-site parking and yards. A single-family home is likely the best fit.

The lock-and-leave professional

You want convenience, security and on-site services. You travel, host guests in amenity spaces and prefer walkability to Harvard, Central or Kendall. A well-run condo with concierge and garage parking can maximize your time and reduce upkeep.

The investor or part-time resident

You want a property that stays liquid with a wide buyer pool and predictable monthly costs. A centrally located 1–3 bedroom condo can be a good match. Review rental policies, reserve levels and special assessment history to manage risk.

Your due-diligence checklist

Use this list before you commit, then plug numbers into the worksheet above.

- Condos: HOA budget, most recent reserve study or statement, monthly dues, master insurance, 12–24 months of meeting minutes, special assessment history, occupancy and rental rules, master deed and bylaws, management contract and any engineering reports. Review state reserve requirements via Massachusetts reserve guidance and reserve funding overview.

- Single-family: Seller disclosures, City inspection and permit history, roof/HVAC/structural reports when available. Use the City’s FY26 tax rate of $6.67 per $1,000 to model taxes and confirm assessed value via the Assessing Department.

- Parking: Confirm deeded or assigned spaces and eligibility for resident permits through the City’s parking permit rules. If no space is included, get current monthly garage rates nearby.

- Financing: Before going under contract, ask your lender to confirm the building’s project review status and any limitations. See the condo project review guide for what lenders check.

How to decide, step by step

- List your non-negotiables. Examples: private yard, on-site parking, concierge, walk-to-work.

- Run the full monthly picture. Use the table to total mortgage, taxes, HOA, insurance, maintenance and parking for each option.

- Stress-test HOA risk. Read minutes, reserves and engineering reports for signs of major capital work.

- Confirm financing. Make sure the condo is eligible for your loan type or line up a portfolio option.

- Walk the blocks. Use the City’s neighborhood map to match location and lifestyle.

- Think five years out. Consider how your needs and resale timing could change.

Ready to weigh specific addresses and numbers? You can get a neighborhood-level, fully loaded cost comparison and building review tailored to you. Connect with Sandrine Deschaux to map your best path in Cambridge.

FAQs

What is Cambridge’s current property tax rate and how do I estimate my monthly bill?

- The FY26 residential rate is $6.67 per $1,000 of assessed value. Multiply the assessed value by 0.00667 to get the annual bill, then divide by 12; see the City’s tax rate summary.

How do condo special assessments work and how can I gauge the risk?

- Boards can levy assessments for major repairs when reserves fall short; review reserves, budgets and minutes to spot upcoming projects and read a Massachusetts reserve overview.

What does “warrantable” mean for a Cambridge condo and why does it matter?

- Warrantable projects meet lender and agency standards for reserves, insurance and project health; non-warrantable status can limit financing options, so ask your lender early and see this condo project review guide.

Are parking spaces standard with Cambridge condos?

- No. Many older conversions lack deeded spaces; plan for resident street permits or a monthly garage if needed and review City parking permit rules.

Are single-family homes harder to find in West Cambridge?

- Yes. Inventory is limited and demand is strong for larger lots and historic homes, which concentrates competition and supports higher price points in that submarket.